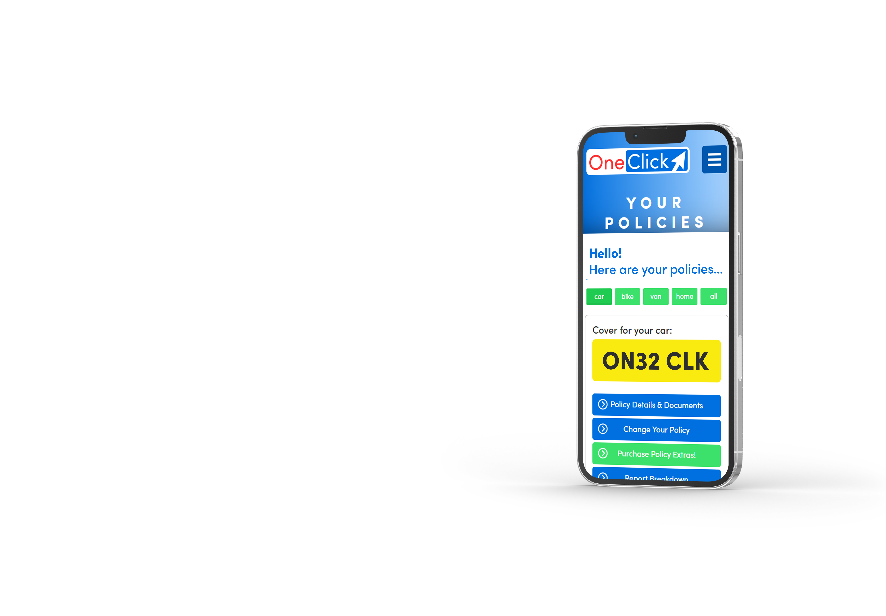

Managing your policy online…

One Click is a Fully Self Service Insurance Company. Upon purchasing your policy you’ll be provided with an online portal so you can manage your policy at any time and place that’s convenient for you.

One Click is a Fully Self Service Insurance Company. Upon purchasing your policy you’ll be provided with an online portal so you can manage your policy at any time and place that’s convenient for you.

Make a change to your policy

Make a change to your policy- Make a payment

- Make a claim

- Review your renewal

- View and download your policy documents

- 24 hour emergency claims phoneline

Looking to add a little more to your policy?

Our aim is to get you a policy that saves you both time and money, but if you’re looking for a little more then we’ve got you covered! Explore our policy extras in your customer portal today…